Property rights in Corsica in disarray

The Senate has adopted, on first reading, the bill to extend the period of validity of the law no. 2017-285 of 6 March 2017 on cadastral remediation and clearing up property disorder.

In particular, this law includes exemptions to facilitate the use of notarial deeds for goodwill to prove ownership of a property located in Corsica, as well as tax exemptions on inheritance tax, applicable until 31 December 2027.

The text proposes to extend for 10 years these provisions, sor until 31 December 2037.

What you also need to know:

I.- Proposal for a law to extend Law No. 2017-285 of 6 March 2017 on the reorganisation of cadastral registers and the elimination of property clutter

The sole article of the proposed law aims to extend, for a period of ten years, i.e. until 31 December 2037, the civil and tax derogations applicable to Corsica in matters of inheritance provided for by Law no. 2017-285 of 6 March 2017. relating to cadastral reorganisation and the elimination of property clutter.

Taking the view that, despite the progress made since 2017 and because of the incomplete nature of the work, the titling work carried out in Corsica should be supported, the committee adopted this article without amendment.

Act 2017-285 of 6 March 2017, a tool to encourage the titling of Corsican land

a) A specific feature of Corsica: a land disorder that is detrimental to the island's development

Corsica is characterised by a higher rate of property for which the legal title does not correspond to the reality of its ownership or possession than the rest of France, due in particular to the following factors the absence of title deeds, the inaccuracy of the land register and the perpetuation of many situations of joint ownership of estates. This disorder is the result of the territory's cultural and historical particularities, as well as the special tax regime that Corsica has benefited from since the «Miot» decree of 1801.

André-François Miot was appointed to Corsica to improve the island's administrative and legal situation, particularly as regards the collection of inheritance tax. introduced in 1801 an inheritance tax system for Corsica that derogates from ordinary law, in the face of the fact that the local population's standard of living did not allow it to comply with national tax standards.

Article 3 of the Miot decree of 10 June 1801 created two exceptions to the general law of inheritance in order to encourage Corsicans to regularise their property situation. On the one hand, the, the method of calculating inheritance tax was adjusted so that the value of real estate was assessed not on the basis of its actual value, but on the basis of one hundred times the amount of the State's share of the property contribution, This allows the tax value of properties to be reduced to 1 to 2 % of their market value. The decree also provides for the repeal of penalties for failure to declare estates, Under common law, this is incurred six months after the death of the owner.

The derogation system created by the Miot decree, in force until 1949, led to the end of declarations of inheritance due to the absence of penalties, and thus contributed to the proliferation of situations of joint ownership or related owners., who have been dead for several years.

In addition to the disincentives created by this distinct tax system, the land disorder is also reinforced by the socio-economic development of Corsica over the course of the 20th century.e century. The significant loss of life on the island during the First World War contributed to abandonment of plots, The land was gradually rendered unusable by the expansion of the maquis. With no prospect of exploiting their land, the new generations of Corsicans began a major rural exodus in the 1930s, speeding up the loss of title, indivision and failure to demarcate property in rural and mountainous areas.

In 1983, the commission on joint ownership, set up on the initiative of the then Minister of Justice, Robert Badinter, and tasked with studying joint ownership in Corsica, found that the particularly low sharing rate on the island, joint ownership of 14.8 % of built-up properties and 39 % of undeveloped properties. Noting that the land disorder resulted, on the one hand, from the absence of title deeds and, on the other hand, from the absence of inheritance declarations, The commission's conclusions encouraged notaries to develop the use of notoriété acquisitive deeds and recommended the adoption of tax incentives to encourage citizens to regularise joint ownership or inheritance situations.

The absence of title deeds and the perpetuation of joint inheritance have multiple consequences for citizens and public authorities alike.

These situations deprive usufructuaries of the full exercise of their right of ownership, in particular in respect of gifts inter vivos, the settlement of an estate or the conclusion of a sale or lease, and place them in a situation of legal uncertainty, This limits the incentive to preserve and maintain their property.

On an island-wide scale, the increasing number of unsettled estates is leading to degradation of land and property as well as a shortage of property which can contribute to a rise in prices. It is therefore up to local authorities to deal with the consequences of abandoning certain built-up properties, both in terms of managing the risks involved and the challenges of reducing housing capacity.

For the public authorities, land disorder also leads to a loss of tax revenue and can limit the ability of local authorities to maintain their land. The impossibility of identifying owners also leads to difficulties in applying certain standards, such as the legal obligations to clear undergrowth.

As a result, a number of measures have been taken since the 1980s, starting with tax measures and continuing with civil and administrative measures.

Firstly, the special tax arrangements were amended by Act No. 98-1266 of 30 December 1998. of the 1999 Finance Act which abolished the exemption from penalties for failure to declare an inheritance. However, the return to ordinary law was systematically postponed by the Finance Acts until a new derogation regime was established. by Law 2002-92 of 22 January 2002 relating to Corsica which provides the exemption from inheritance tax of 50 % of the value of the property and sets the deadline for declaring the inheritance of a property in Corsica at twenty-four months. The Supplementary Finance Act No. 2008-1443 of 30 December 2008 extended these measures until 2017.

Secondly, in view of the number and difficulty of the cases, a public interest group was set up in 2006 to assist notaries and heirs with the task of reconstructing titles.

The public interest group for the reconstitution of property titles in Corsica (GIRTEC)

Article 42 of Law no. 2006-728 of 23 June 2006 created the public interest group for the reconstitution of property titles in Corsica (GIRTEC) for an initial period of ten years, tasked with gathering all the information needed to reconstitute title deeds for land and property without them.

The State, the territorial collectivity of Corsica, the association of mayors of Corse-du-Sud, the association of mayors of Haute Corse and the regional council of notaries of Corsica, ex officio members, administer the grouping and ensure that it has the necessary resources to carry out its tasks. The public interest grouping therefore receives financial contributions from its members to its annual budget, mainly made up of the State's financial contribution as part of the exceptional investment programme (PEI) for Corsica until 2020, followed by a State grant awarded in February 2024. The group also benefits from the provision of staff, premises and equipment by its members, enabling it to draw on a team of ten agents to respond to referrals and conduct the resulting research.

Under the terms of the 2007 and 2017 founding agreements, GIRTEC has two missions:

- the public interest group is responsible for gather together all the information needed to reconstitute the property titles in Corsica for land and property that does not have one and may in this respect «.« to take any measure enabling these assets to be defined and their owners to be identified, and to create or manage all facilities or services of common interest made necessary to achieve its purpose ». It therefore has a right of communication with any person, natural or legal, under private or public law, enabling it to obtain all documents and information necessary to carry out this mission, without being bound by professional secrecy. Without taking the place of notaries in the establishment of a title deed, GIRTEC is therefore called upon by the latter to carry out research and enable them to create a title deed (notoriété acquisitive) or to have it legally entered into municipal assets;

- GIRTEC's constitutive agreement, as amended in 2017, following the group's continued existence, also entrusted it, in addition to the requests made by persons directly interested in the reconstitution of property titles, with the possibility, exclusively at the service of public persons and establishments, to gather the information needed to identify the owners of land and property in order to provide the information required to carry out their public interest missions.

After two years of defining working methods and collecting data, GIRTEC began its work in earnest in 2011. By 2017, it had helped to restore more than 3,264 property titles, at an average rate of 500 cases processed each year..

After focusing on the titling of property belonging to private individuals, since 2022 the group has been developing assistance with the titling of property belonging to local authorities. An agreement was signed in November 2023 with the two associations of mayors and the regional council of notaries to help with the titling of communal plots for which no title exists.

In 2016, the General Council for the Environment and Sustainable Development's working group on combating land pressure and property speculation in Corsica, set up at the request of the Prime Minister, welcomed advances made possible by the work of GIRTEC. He did, however, mention the persistence of land disputes, particularly with regard to the high proportion of properties that are still undefined, representing 15.6 % of the island's registered surface area, and plots where the owner is presumed deceased, representing 35 % of the plots. He pointed out that « The elimination of land tenure problems requires the use of three complementary tools: technical tools (GIRTEC's work to reconstitute title deeds), civil tools (the notary's deed establishing ownership) and fiscal tools (payment of inheritance tax). ".

As a result, the working group's conclusions called for making the usucapion procedure more secure and effective by reducing deadlines and enshrining it in law, and also advocated the continuation of GIRTEC, This is in recognition of the fact that it will take several more decades of work to reconstitute title deeds in order to clear up the land confusion.

b) In response to the « land disorder »In the wake of the "death crisis" in Corsica, Act No. 2017-285 of 6 March 2017 introduced and extended derogations from the inheritance system for a period of ten years.

In order to resolve, or at least improve, the situation by providing legal and tax solutions to the structural problem of the disorganisation of Corsican land, the legislature adopted Act no. 2017-285 of 6 March 2017, on the proposal of the former deputy for Corse-du-Sud, Camille de Rocca Serra. relating to cadastral reorganisation and the elimination of property clutter.

This law contains six articles, five of which, articles 1er 5, concern Corsica or the whole of France. These articles are intended to apply for a period of ten years: as the law currently stands, they will therefore expire on 31 December 2027.. Article 6, inserted by the Senate Law Committee at the suggestion of its rapporteur, André Reichardt, is a permanent provision applicable in Alsace-Moselle. It is not affected by the extension proposed in this bill.

II. Act No. 2017-285 of 6 March 2017 to promote cadastral reorganisation and the elimination of property disorder

Article 1er

When a notarial deed of notoriety relates to a property located in Corsica and establishes possession that meets the conditions of prescription, it is proof of possession, unless proven otherwise. It may only be contested within a period of five years from the last of the publications of this deed by means of posting, on a website and at the land registry office.

This article applies to notarial deeds drawn up and published before 31 December 2027. The said deeds are exempt from land registration tax.

A decree in the Conseil d'Etat shall set out the conditions for the application of this article.

Article 2

For joint ownership established by a notarial deed of notoriety drawn up under the conditions set out in Article 1er of this law, in the absence of an existing title deed, the undivided co-owner(s) holding more than half of the undivided rights may perform the acts provided for in 1° to 4° of article 815-3 of the Civil Code.

However, the consent of the undivided co-owner(s) holding at least two-thirds of the undivided rights is required for any act that does not relate to the normal operation of the undivided property and for any act of disposal other than those mentioned in 3° of the same article 815-3.

The undivided co-owner(s) must inform the other undivided co-owners.

Article 3

In the first paragraph of 8° of 2 of Article 793 of the General Tax Code, the rate: «30 %» is replaced by the rate: «50 %» and, at the end, the year: «2017» is replaced by the year: «2027».

Article 4

The I of article 1135 bis of the same code is amended as follows

1° In the second paragraph, «2017» is replaced by «2027»; ;

2° In the last paragraph, «2018» is replaced by «2028».

Article 5

C of V of Section II of Chapter I of Title IV of Part One of Book Ier of the same code is supplemented by an article 750 bis B as follows:

«Art. 750 bis B.-Between 1er Between 1 January 2017 and 31 December 2027, deeds of partition of inheritance and licitations of hereditary property meeting the conditions set out in II of Article 750 are exempt from the duty of 2.5 % up to the value of the property located in Corsica.»

Article 6

Article 24 of the law of 31st March 1884 concerning the renewal of the land register, the equalisation of property tax and the conservation of the land register in the departments of Moselle, Bas-Rhin and Haut-Rhin is amended as follows:

1° The third paragraph reads as follows

«The first two paragraphs are without prejudice to the application of Title XXI of Book III of the Civil Code; ;

2° The last paragraph is deleted.

Articles 1er and 2 concern civil law and introduce derogations from the rules of inheritance and joint ownership. in order to encourage the titling of plots of land and to facilitate the management of joint ownership resulting from old and poorly documented successions, which therefore include a large number of joint owners. Articles 3 to 5 provide for tax exemptions, introduced in 2017 as incentive measures aimed, once again, at supporting the reconstitution of title deeds and the withdrawal from joint ownership. However, they are broader in scope, as they also apply to successions of titled property, with no particular difficulties.

III. Civil derogations from the law of succession

Article 1er Act No. 2017-285 introduced a derogation from the Civil Code, by facilitating the use of notarial deeds of acquisitive notoriety to prove possession of property located in Corsica. The aim was to provide legal certainty for titling procedures, while Corsican notaries have been using deeds of notoriété acquisitive since the 1980s.

Acquisitive prescription, as defined in article 2258 of the Civil Code, is «.« a means of acquiring property or a right by the effect of possession without the person alleging it being obliged to produce title thereto or that the exception of bad faith can be invoked against it ». It can only be implemented if the conditions set out in article 2261 of the same code are met: it presupposes « continuous and uninterrupted, peaceful, public, unequivocal possession as owner ». This possession must be long-term: article 2272 of the same code specifies that «.« the limitation period required to acquire ownership of real estate is thirty years ".

In practice, the statute of limitations only takes effect if it is invoked by the possessor as a defence to the claim brought by the person claiming to be the true owner of the property.

A notarised deed of notoriety is therefore a probationary tool. It provides material evidence that the beneficiary's possession, in terms of its duration and characteristics, meets the conditions for acquisitive prescription. Once acquired, prescription has the effect of making the possessor the owner of the property.

The provisions of Article 1er of Law 2017-285 is derogates from ordinary civil law insofar as the practice of notarial deeds of acquisitive notoriety is formally authorised by the legislator only for Corsica and limits the period during which the deed of acquisitive notoriety may be contested to five years, The five-year period begins on the date of the last of the publications of this act by posting in the town hall, on the website of the prefecture and the Corsican local authority and at the land registry office. However, it should be noted that only the action against the deed of notoriété acquisitive is subject to this five-year time limit It is therefore always possible to bring an action to reclaim the property. However, now that the notoriété acquisitive deed has become incontestable, it is theoretically more difficult to prove that the possessor is not in the right.

Article 66 of the Finance Act 2022-1726 of 30 December 2022 also added the following to this article exempt these notarised deeds of notoriété acquisitive from the taxe de publicité foncière (land registration tax).

Article 2 of Law 2017-285 also derogates from ordinary civil law, more specifically Article 815-3 of the Civil Code, insofar as it provides for separate majority rules for the management of undivided interests established by a deed of notoriety drawn up under the conditions set out in Article 1er of law no. 2017-285.

Article 815-3 of the Civil Code

The undivided co-owner(s) holding a’at least two thirds of undivided rights may, at that majority :

1° To carry out acts of administration relating to undivided property; ;

2° Give one or more undivided co-owners or a third party a general administration mandate ;

3° Sell the undivided movable property to pay the debts and charges of the joint ownership; ;

4° Concluding and renewing leases other than those for agricultural, commercial, industrial or craft use.

They must inform the other undivided co-owners. If they fail to do so, any decisions taken will not be binding on them.

However, there are a number of reasons for this, the consent of all the undivided co-owners is required for any act that does not relate to the normal use of the undivided property and for any act of disposal other than those referred to in 3°.

If an undivided co-owner takes over the management of the undivided property, with the knowledge of the others and nevertheless without opposition from them, he is deemed to have received a tacit mandate, covering acts of administration but not acts of disposal or the conclusion or renewal of leases.

In effect, it reduces to a simple majority, A two-thirds majority is required under ordinary law, the threshold required to perform the administrative acts essential to the proper management of the property. Likewise, it lowers to a two-thirds majority, This is in contrast to the unanimity rule under ordinary law, the threshold required to carry out acts of disposal, such as sales or transfers.

ii. Tax exemptions to encourage the reconstitution of property titles

Articles 3 to 5 of Law 2017-285 supplement the civil provisions by adding tax exemptions.

In order to encourage users of property for which title deeds do not exist to take steps to regularise their situation, Article 3 amended article 793 of the General Tax Code, in order to extend the partial exemption from free transfer duties by ten years (applicable to gifts and inheritances) on the first transfer subsequent to the reconstitution of the relevant property titles and secondly, to increase this exemption to 50 % of the value of the property, compared with 30 % previously.

Article 793 of the General Tax Code (extracts)

The following are exempt from transfer duties:

[...]

8° Buildings and property rights, up to 50 % of their value, on the first transfer subsequent to the reconstitution of the property titles relating thereto, provided that such title deeds have been duly transcribed or published between 1 January and 31 December.er October 2014 and 31 December 2027.

This exemption is exclusive of the application to the same property, in respect of the same transfer or a previous transfer, of any other exemption from transfer tax.

This exemption applies to the whole of France, The new law applies to the French overseas territories and Corsica, which are more affected by the lack of title deeds. As the law currently stands, it applies to title deeds that have been duly transcribed or published between 1 January and 31 December.er October 2014 and 31 December 2027.

It should be noted that this tax advantage cannot be combined with with other free transfer tax exemptions, in particular the inheritance tax exemption provided for in Article 4.

Article 4 Act no. 2017-285 amended article 1135 bis of the General Tax Code, in order to extend the derogation on inheritance tax by ten years, which was set up in 2002 on a transitional basis, which applies a partial exemption from inheritance tax of 50 % to property located in Corsica..

Article 1135 bis of the general tax code

I. - Subject to the provisions of II, for estates opened between the date of publication of law no. 2002-92 of 22 January 2002 relating to Corsica and 31 December 2012, property and property rights located in Corsica are exempt from death duties.

For estates opened between 1er Between 1 January 2013 and 31 December 2027, the exemption mentioned in the first paragraph applies to half of the value of the property and property rights located in Corsica.

For estates opened on or after 1er From 1 January 2028, immovable property and rights to immovable property situated in Corsica will be subject to death duties under the conditions of ordinary law.

II. - These exemptions do not apply to immovable property and rights to immovable property for which the deceased's right of ownership has not been established prior to his death by a duly transcribed or published deed unless the notarised certificates mentioned in 3° of article 28 of decree no. 55-22 of 4 January 1955 reforming land registration relating to this property are published within twenty-four months of the death.

This exemption applies to inheritances of property located in Corsica, including those for which there are no particular titling difficulties. As the law currently stands, it is, applicable until 31 December 2027, the ordinary law on inheritance tax will apply., for the first time since the Miot decree of 1801, apply in Corsica from 2028.

And finally.., Article 5 Act No. 2017-285 introduced a new article 750 bis B in the General Tax Code, in order to reinstate, for a period of ten years, an exemption from inheritance tax on real estate located in Corsica. This is the same measure as that set out in article 750. bis A of the same code, which only applied between 1 January and 31 December 2006.er This period, which ran from 1 January 1986 to 31 December 2014, could not be extended due to a ruling by the French Constitutional Council.

Article 750 bis A of the General Tax Code

Deeds of partition of an estate and licitations of hereditary property meeting the conditions set out in II of Article 750, drawn up between 1 January and 31 December, are subject to the same conditions as the deeds of partition and licitations of hereditary property.er Between 1 January 1986 and 31 December 2014, the value of property located in Corsica is exempt from the 2.50 % duty. These exemptions apply provided that the deed is notarised and specifies that it has been drawn up under the terms of IV of article 11 of law no. 85-1403 of 30 December 1985.

Article 750 bis B of the General Tax Code

Between 1er Between 1 January 2017 and 31 December 2027, deeds of partition of inheritances and licitations of hereditary property meeting the conditions set out in II of article 750 are exempt from the 2.5 % duty up to the value of property located in Corsica.

The exemption provided for in article 750 bis B concerns all estates in Corsica, including those for which there are no particular titling difficulties. As the law currently stands, it is, applicable until 31 December 2027.

Under ordinary law, partition duties are payable when, following the settlement of an estate, the heirs choose to put an end to their joint ownership by signing a deed of partition, which allocates certain assets to them. Under the terms of article 750 of the General Tax Code, taxpayers who carry out this act of partition must are subject to registration duty or land registration tax of 2.50 % when the succession is in favour of the original members of the joint ownership, their spouses, their ascendants or descendants or the universal beneficiaries of one or more of them.

IV. The Senate's position in 2017: unanimous support for the text despite reservations about tax exemptions

Act 2017-285 was adopted with the support of the Law Commission and then, in the public session, of all the political groups. represented at the time in the Senate, albeit with a number of reservations, in particular about the text's tax provisions.

Articles 1er and 2 were adopted unanimously, after a number of editorial changes and a refocusing of the scheme on Corsica, at the initiative of the rapporteur. The committee had confirmed « the particularly problematic land situation in Corsica »and invited the Senate to« approve the objectives of the proposed law ». In so doing, the committee considered that « although [these] article[s] are very different from ordinary law, they meet a real need and, [...] without this flexibility, GIRTEC's work would be ineffective. ".

On the other hand, the tax articles - 3 to 5 - raised a number of questions, particularly from the Finance Committee, which was asked to give its opinion on the text.

The Finance Committee identified several legal difficulties with these three articles. Firstly, it felt that the ten-year period provided for in the text was excessive, in view of the practice whereby tax expenditure should only be renewed for three-year periods. Secondly, it pointed out that two of the three tax provisions set out in the text - Articles 4 and 5 - apply to all properties, including those that are demarcated and whose owners are known. The Finance Committee therefore considered that « the provisions set out in Articles 4 and 5 of the proposed law reveal major weaknesses with regard to the constitutional principle of equality before the law "1(*).

These weaknesses are supported by the case law of the Constitutional Council, which has twice declared provisions similar to those in Articles 4 and 5, which had been introduced in Finance Acts, to be contrary to the Constitution. In its decision of 29 December 2012 on the 2013 Finance Bill2(*), the Constitutional Council ruled that « the maintenance of the special tax regime applicable to inheritances of real estate located in the departments of Corsica means that, without any legitimate reason, the transfer of such real estate may be exempt from the payment of transfer duties; that the new extension of this special regime infringes the principle of equality before the law and public burdens ». The same decision was handed down when the Constitutional Council examined the Finance Act for 2014.3(*). On the other hand, the Constitutional Council did not raise any grounds of unconstitutionality in relation to 8° of 2 of Article 793 of the General Tax Code (amended by Article 3 of Law 2017-285).4(*).

While noting these reservations, the Law Commission nevertheless pointed out that the Constitutional Council had also ruled that «.« the principle of equality does not preclude the legislature from regulating different situations in different ways or from derogating from equality for reasons of public interest, provided that, in either case, the resulting difference in treatment is directly related to the purpose of the law establishing it "5(*). The committee considered that the land disorder that has been structuring Corsica for more than two years constituted «.« a different situation »These derogations also exist for the overseas territories. Such derogations also exist for the overseas territories, and have recently been strengthened by Article 14. bis of the bill on speeding up and simplifying the renovation of run-down housing and major development projects6(*).

c) A satisfactory but incomplete assessment of Act 2017-285

Seven years after its implementation, Law No. 2017-285 shows that fairly satisfactory results, although the deadline for completing the titling work still seems a long way off.

From a qualitative point of view, neither the notaries of Corsica nor the Department of Civil Affairs and the Seal (DACS) of the Ministry of Justice have informed the rapporteur of any litigation difficulties relating to the application of Articles 1 and 2 of the Act.er and 2 of Act no. 2017-285.

From a quantitative point of view, titling work has progressed, This has led to a reduction in the number and proportion of plots in the name of presumed deceased owners.

According to figures provided to the rapporteur by GIRTEC, 1,868 titles created between 2018 and mid-March 2024. On average, a title covers 7.72 plots, at least 15,000 plots of land have been titled since the adoption of law no. 2017-285. When questioned by the rapporteur, the Corsican Regional Council of Notaries indicated that these titling operations had undoubtedly been encouraged by the derogations opened up by this law, and in particular by Article 1.er which guaranteed the legal validity of notarised deeds of acquisitive notoriety. From the point of view of its appropriation by local players, Act 2017-285 is therefore a tool that has been used, demonstrating that it meets a real need.

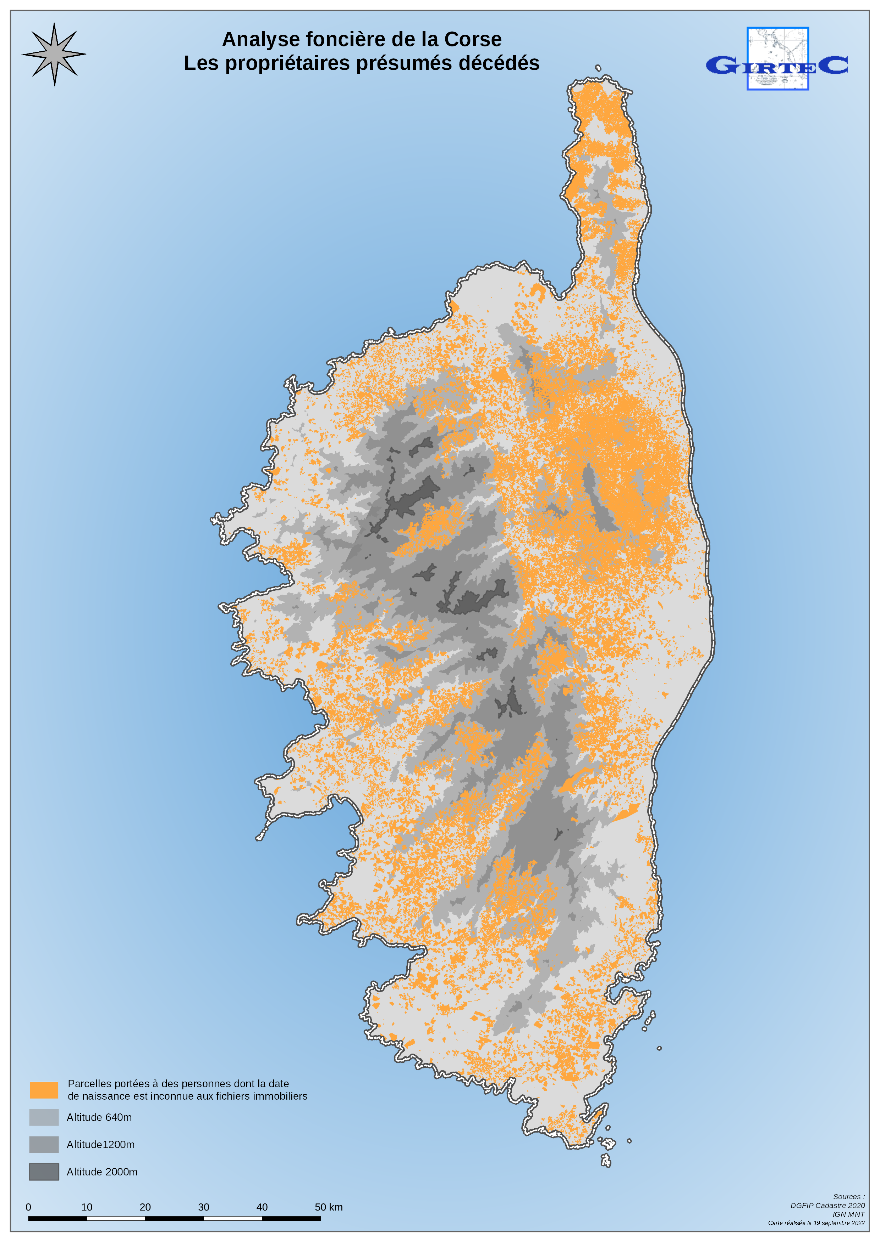

According to GIRTEC, the current number of plots of land in the name of presumed deceased owners is 313,323, i.e. 30.4 % of the 1,030,951 plots on the island. It is therefore a question of’a drop of 4.6 percentage points compared to the situation prior to the passing of Law 2017-285 (see above) and’a fall of more than ten percentage points compared with 2009, At that time, 405,727 of the 995,386 plots of land on the island belonged to presumed deceased owners, or 40.8 %. The fall, in proportion, is actually more marked if the increase in the number of plots (+ 35,000) is taken into account, which has changed the denominator. This increase in the total number of plots is partly the result of titling operations, as newly titled plots may have been resold or divided up. All in all, compared with 2009, there were almost 100,000 plots no longer considered to belong to a presumed deceased owner, This represents a quarter of the number of such plots recorded in 2009. Map of plots belonging to presumed deceased persons (2020).

Source: GIRTEC, based on 2020 data

Although it can't be described as fast, this downward trend is nevertheless real and significant, This is all the more true given that, as the cases posing the fewest difficulties are resolved and there are fewer living witnesses able to attest to prescription of ownership in villages suffering from depopulation, the parcels that remain to be titled are the most delicate to deal with, both for notaries and for GIRTEC. In particular, property that has not been demarcated, where progress has been slower, appears to be more complex to deal with, as the absence of a title entangles with the difficulty of reconstituting the demarcation of plots without harming the rightful claimants.

Valuation of tax items (Articles 3 to 5 of Act no. 2017-285) is more uncertain. When questioned by the rapporteur, the Directorate General of Public Finances (DGFiP) was unable to provide data, even approximate data, on the cost of the tax exemptions they provide. Partial exemption from inheritance tax for properties in Corsica, provided for in article 1135 bis of the General Tax Code as amended by Article 4 of Act no. 2017-285, has been estimated at 20 million euros in Volume II of the «Ways and Means» document appended to the Finance Bill for 2024. This sum should be compared with the total amount of duties collected in respect of inheritance declarations filed in Corsica, which amounted to €43.6 million in 2022.7(*). This amount appears to have risen in recent years, since it amounted to 32.6 million euros in 2018, an increase of 33.7 %. GIRTEC believes that this increase in inheritance tax receipts in Corsica can be explained by «the following factors« necessarily »This is why the tax aspect of Act no. 2017-285 was considered by the Corsican Regional Council of Notaries and the GIRTEC as not detachable from the derogations from civil law opened up by the Act. This is why the tax component of Act 2017-285 was considered by the Corsican Regional Council of Notaries and GIRTEC not to be detachable from the derogations from civil law opened up by the said Act. However, this analysis was not corroborated by the DGFiP.

In any case, all these factors, however partial, demonstrate that efforts to register and demarcate plots of land must continue, This was unanimously recognised by all those interviewed by the rapporteur. In this respect, the timeframe of 20 to 30 years for normalising the cadastral situation in Corsica mentioned in the report by the working group «Combating land pressure and property speculation in Corsica», drawn up in June 2016, still seems fully relevant.

GIRTEC, the Corsican Regional Council of Notaries and the DACS have supported the principle of extending Law 2017-285.. In particular, GIRTEC considered that « the 2027 deadline was set on the basis of an unachievable objective. In fact, it was impossible to envisage clearing up a two-century old land mess in just a few years.. [...] The Act of 6 March 2017 created a momentum that must be maintained ".

V.- The proposed law aims to extend, for ten years, the civil and fiscal derogations applicable to Corsica in matters of inheritance.

Arguing that « need to adapt the law in order to reduce the number of [the] property disorder »The author of the draft law wishes to extend the application of Act 2017-285 by ten years of 6 March 2017. This would therefore apply until 31 December 2037., Under current law, the deadline is 31 December 2027.

To this end, Article I of the sole article of the proposed law amends Article 1.er of Law no. 2017-285 by replacing the year «2027» with the year «2037». The effect of this amendment is to extend, for the period, the application of Article 2 of Law no. 2017-285.

II of the sole article of the proposed law directly amends the General Tax Code in order to extend the tax exemptions provided for by Law 2017-285 until 2037:

- 1° amends article 750 bis B of the General Tax Code, which had been inserted by Article 5 of Law 2017-285 ;

- 2° amends 8° of 2 of Article 793 of the General Tax Code, which had been amended by Article 3 of Law 2017-285 ;

- finally, 3° amends article 1135 bis of the General Tax Code, which had been amended by Article 4 of Law 2017-285.

III of the sole article of the proposed law is a financial pledge to compensate the State for the loss of revenue resulting from the extension of tax exemptions.

VI - A still incomplete titling movement, to be supported by the extension of Law 2017-285 of 6 March 2017

Although gradually rising, the proportion of Corsican plots of land with a legal title deed, of the order of 70 %, is still too low to consider the situation satisfactory, This is particularly true of national figures, which are in excess of 99 %.

Despite the encouraging results of Law 2017-285, there is still plenty of room for improvement. However, it is unrealistic to expect the situation to return to normal by the current deadline of Law 2017-285, i.e. 31 December 2027., More than 300,000 plots still belong to presumed deceased owners.

This is why the commission felt that the work of titling Corsican land should be supported over the long term. In addition, it noted that the benefits of cadastral reorganisation, both in terms of legal certainty for owners and future tax revenues once these owners are fully identified, outweigh the short- and medium-term cost of the tax exemptions voted in 2017.

The committee therefore approved the draft law, by noting that the extension, until 2037, of Law 2017-235 corresponded approximately to the period of « 20 to 30 years to achieve a healthy situation »Identified in 2016 by the working group« Combating land pressure and property speculation in Corsica ".

The commission adopted the single article without amendment.

* 1 Opinion No. 342 (2016-2017) by Albéric de Montgolfier, on behalf of the Finance Committee, on the proposed law to promote cadastral reorganisation and the reduction of property disorder, submitted on 31 January 2017.

* 2 Decision no. 2012-662 DC of 29 December 2012 on the 2013 Finance Act.

* 3 Decision no. 2013-685 DC of 29 December 2013 on the 2014 Finance Act.

* 4 Decision no. 2014-707 DC of 29 December 2014 on the Finance Act for 2015.

* 5 Decision no. 1996-375 DC of 9 April 1996 on the law containing various economic and financial provisions.

* 6 This bill was adopted by both chambers in identical terms and was awaiting promulgation at the date of publication of this report.

* 7 Based on data supplied by the DGFiP.